Use our debt validation letter to request the validity of a debt.

Updated September 25, 2023

Written by Yassin Qanbar | Reviewed by Brooke Davis

A debt validation letter is correspondence you send to debt collectors and creditors to request proof of the debts. Under federal law, you have a right to get information about any debt you supposedly owe. The law provides a way to send this type of letter to verify the debt collection agency and determine whether it has a legitimate claim.

15 U.S. Code § 1692g(b): Federal law requires that you send a debt validation letter within 30 days of the initial communication from the debt collector. An initial communication is the first time a creditor contacts you, whether this is by phone, a letter, or another method.

A debt validation letter is a document that asks the collector to verify the debt and their authority to collect it. Many debts are sold and resold to various parties, and accurate records are necessary for establishing the debt collector’s rights. These records must also show that you owe the debt.

Before you pay any amount to a debt collector, you’ll want to confirm that the debt belongs to you, as a debt collection company’s records can be inaccurate. You may be charged for a debt that isn’t yours.

You should send a debt validation letter any time you receive a debt collection notice. Even if you think you owe this amount, it’s essential to confirm it. You should also send a debt validation letter if you have any doubts about your allegedly owed debt. You may discover that:

A debt validation letter is an easy way to protect your financial rights. It forces the creditor to do their due diligence and make sure there are no mistakes. If you want to know how to verify a debt collector, sending a debt validation letter is a great way to protect yourself from fraud.

If the debt collector continues to try to collect after failing to send a response, you can report their violations to any or all of the following:

Review these steps to write a concise debt validation letter:

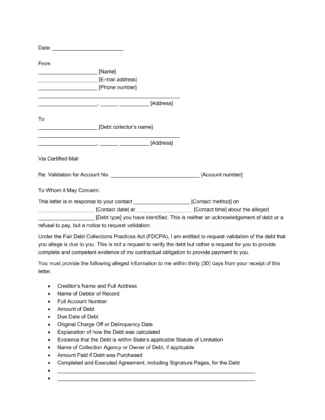

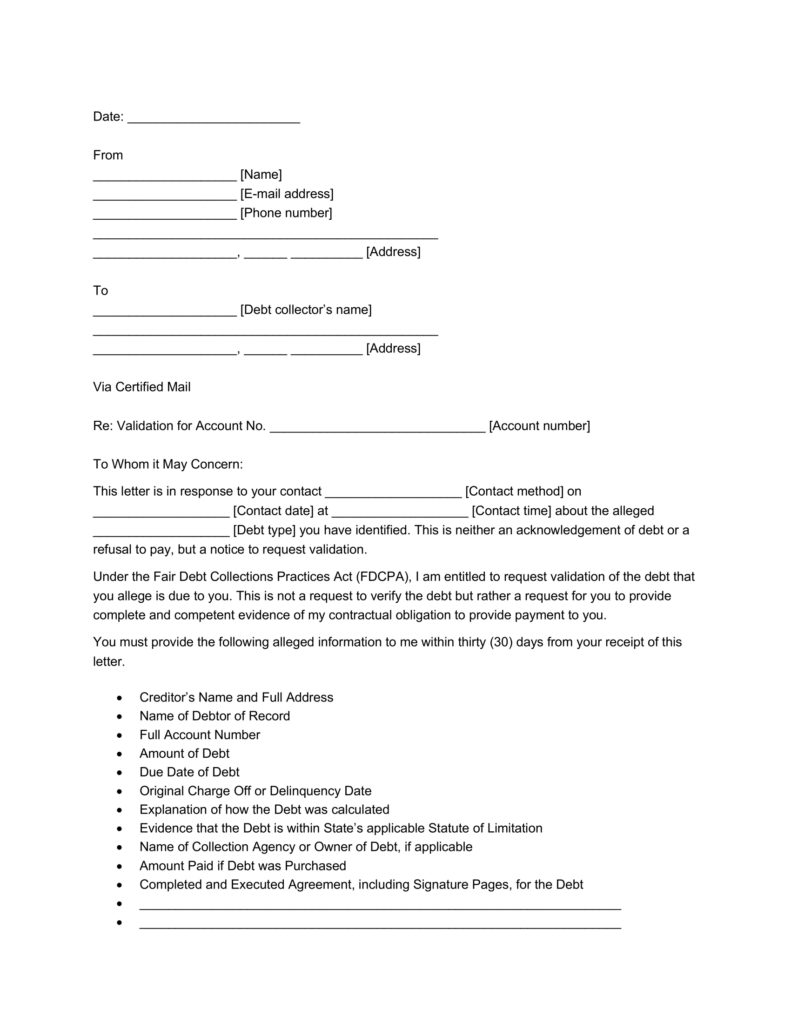

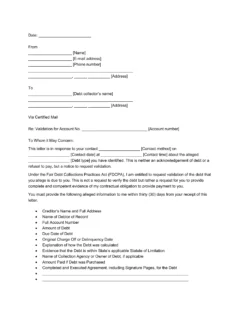

The first step in writing a debt validation letter is filling in your basic information, including your name, email address, phone number, and home address.

You should also fill in the basic information of the debt collector, including their name and contact information.

Then, state the method of communication the debt collector used to contact you:

According to a rule passed by the Consumer Financial Protection Bureau in 2021, a debt collector can contact a consumer via social media about a debt if and only if:

Lastly, provide the date and time the debt collector contacted you.

Specify the type of alleged debt in your letter:

If possible, you should also provide the account number associated with the debt.

Request that the debt collector provide the following information to you:

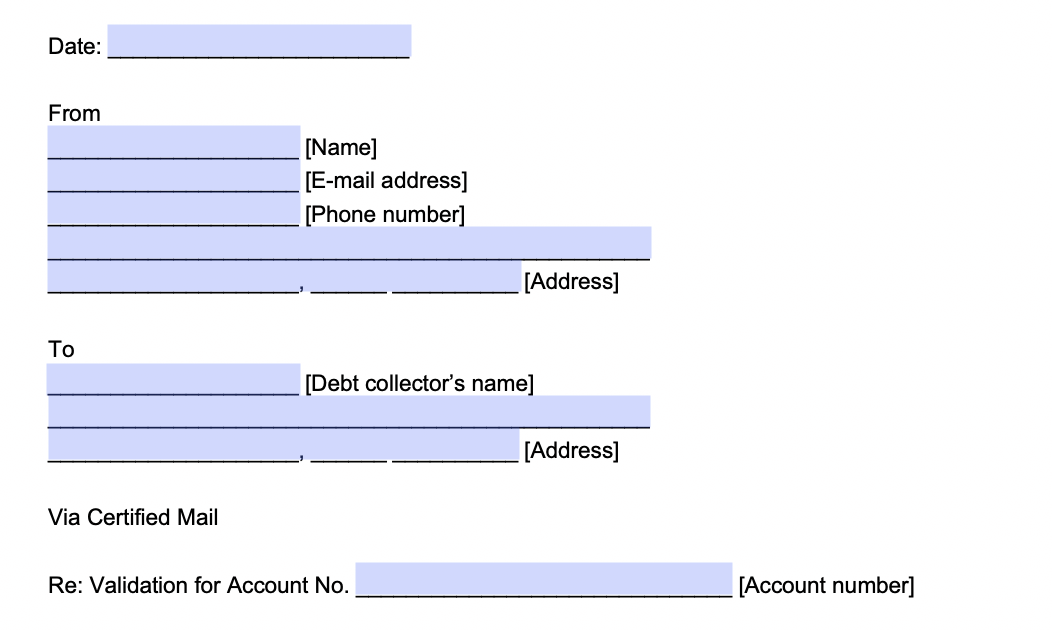

You can also request any additional information you’d like them to provide. Clarify that you’ll be ignoring all other attempts at future collection until they verify that the debt belongs to you. Finish the letter by signing and printing your name.

Follow these steps to send your debt validation letter:

Send your debt validation letter via certified mail. This way, you can create a paper trail and prove that you sent your letter within 30 days of receiving correspondence from the creditor.

Once the creditor receives your letter, they must respond within 30 days. If you don’t get a response within this period, the debt is no longer valid.

If the creditor tries to seek payment without responding, you may need to send a cease and desist debt collection letter.

If you receive a response from a creditor and they confirm your debt, you can review the proof they send to ensure it’s accurate. If the debt is legitimate and the statute of limitations is intact, you can begin making your payments.

View our debt validation letter template below and download it as a PDF or Word file to create your own:

Any further collections are invalid if a debt collector fails to validate the debt letter. These efforts would violate the Fair Debt Collection Practices Act, which governs how debt collectors may act and prohibits unfair, deceptive, and abusive practices. Violations of this act can result in severe repercussions and fines for the debt collector.

If they fail to respond, the debt collector must cease all activities against you, including but not limited to:

Companies often hire collection agencies to collect loan payments, overdue bills, and other debts from consumers. Collection agencies’ sole job is to collect debt, so they are often persistent in their efforts. Therefore, you can protect your financial situation by ensuring these agencies do their due diligence.

Yes. A debt collector may be trying to collect too much from you, so you can dispute part of a debt as long as you specify the details in your debt validation letter.

Create Your Debt Validation Letter in Minutes!